The RBA: What Goes Down Must Come UP

- Evidentia Group

- May 6

- 6 min read

What has happened

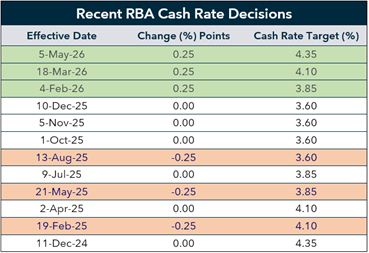

The Reserve Bank of Australia (RBA) today increased the cash rate by 25bp to 4.35%. The move was widely anticipated, with money markets having ascribed approximately a 70% probability to a rate rise today and the clear majority of economic forecasters expecting the same.

Having cut rates three times across 2025, the RBA has now hiked rates three times in succession, in February, March and now in May 2026. The 75bp of easing delivered last year has been entirely reversed, with the cash rate back at its post-pandemic peak of 4.35%.

Eight of the nine Board members voted to increase the cash rate today, while one member voted to leave policy unchanged. This differs from the March Board meeting, when five members voted to raise rates and four voted to keep policy on hold. As such, the Board as a collective has today shifted in a hawkish direction.

At 4.35%, monetary policy is now in restrictive territory, meaning the RBA is deliberately applying the brake to slow the economy. Even if the war in Iran were resolved tomorrow, the effect of higher borrowing costs would slow economic growth and modestly push unemployment higher over the course of 2026. This is intentional. Inflation remains too high, and the central bank's job is to bring it down by cooling demand across the economy.

The ongoing conflict in the Middle East has added a significant layer of uncertainty to the outlook. Notwithstanding, the RBA judged that the policy choice of least regret was to raise rates again, largely because domestic price pressures were already running too hot before the conflict began. The war has simply added to these price pressures.

On that score, the Statement accompanying the Board decision noted that higher fuel prices from the war in the Middle East are “likely to have second-round effects on prices for goods and services more broadly. This inflation impulse is in addition to the high inflation recorded around the start of 2026, reflecting capacity pressures in the economy”.

Inflation: the numbers behind the decision

The RBA has made a material upward revision to its inflation forecasts in its May Statement. The central bank now expects headline CPI, the broadest measure of inflation, to peak at 4.8%/yr in Q2 26, before gradually declining. The trimmed-mean, which strips out the most volatile price movements and is the RBA's preferred measure of inflation, is forecast at 3.8% per year over the same period.

The gap between headline and trimmed mean inflation largely reflects higher fuel prices driven by the war in Iran. Headline inflation is the figure that feeds into wage negotiations, rent reviews and government benefit adjustments each year — and it is the measure that most directly shapes how households feel about the cost of living. The RBA monitors both, but the consequences of elevated headline inflation extend well beyond what the trimmed mean alone captures.

What this means for households

Higher inflation combined with rising interest rates creates double pressure on household budgets. Real household disposable income, that is, what families can actually buy with their after-tax income once inflation is accounted for, is being squeezed from both sides.

The RBA has made a significant downward revision to its forecast for real household disposable income, now expecting growth of just 1.1% per year by the end of 2026, down from a prior forecast of 1.8%.

The impact of rate rises on Australian households is more direct than in many other countries, because most home borrowers here are on variable rate mortgages. When the RBA moves, mortgage repayments move quickly. The upshot is that the three rate rises since February will start to bite, and with consumer sentiment at historically low levels, the confidence effect can amplify the real impact further. The net result is weaker household spending, particularly in discretionary categories, which will weigh on earnings growth and company profits through 2026.

The RBA in a global context

Australia stands somewhat apart from other major economies right now. In the United States, Eurozone, United Kingdom and Canada, central banks have not reversed their rate cuts, and last week all four left rates unchanged. Japan has continued its own shallow tightening cycle, but has moved only in one direction. Since the war in Iran began, market expectations for the major global central banks have shifted in a more hawkish direction — pricing in fewer cuts and potentially more hikes — but none have yet acted on it.

This divergence has a direct consequence for the Australian dollar. As Australian interest rates rise relative to those abroad, the yield advantage of holding Australian dollar assets increases, attracting capital inflows and pushing the currency higher. The AUD has appreciated approximately 7% against the US dollar since the start of the year.

What this means for investors

Today's rate rise was expected, and markets had already adjusted prices in anticipation. The immediate reaction is therefore likely to be contained. Financial markets have priced a peak in the RBA cash rate of 4.7% (i.e. another 35bp of policy tightening). That pricing reflects the balance of risks around the outlook for inflation and the RBA’s concerns around longer-term inflation expectations adjusting higher. The more important question is what the economic environment taking shape over 2026 means for investment portfolios.

For Australian shares, the combination of slowing growth, higher borrowing costs, and weaker consumer spending creates a more challenging backdrop for company earnings. Businesses with significant exposure to domestic discretionary spending, such as retailers, consumer services and media, face the most direct headwind. The financial sector, the largest on the ASX, is more nuanced. Higher rates can support bank profitability in the short term by widening the margin between what banks earn on loans and pay on deposits, but a slowing economy, softer credit growth and the prospect of rising loan defaults present a meaningful offset. Sectors less sensitive to the domestic economic cycle, such as resources and healthcare, may prove more resilient. Investors should expect earnings growth in Australia to moderate through 2026.

On the other side of the ledger, with the cash rate back at 4.35%, the income available from defensive assets, including term deposits, bonds and cash, has improved materially. For more conservative portfolios or for investors looking to increase their defensive allocation, the returns available without taking significant risk are meaningfully better than they were two years ago.

More broadly, monetary policy works with a lag. The full economic impact of the three rate rises in 2026 has not yet fully flowed through to households and businesses. This is not a reason to panic, but it is a reason to remain disciplined and focused on long-term fundamentals rather than short-term noise. History shows that well-diversified portfolios are built precisely for environments like this one. Periods of economic adjustment are uncomfortable, but they are a normal part of the investment cycle, and they pass.

We’re here to support you through all market conditions. If you have any questions or would like to discuss anything about your portfolio in more detail, please don’t hesitate to reach out.

The information contained in this document is provided by Evidentia. Evidentia means Evidentia Group Holdings Pty Ltd ACN 665 634 382 and its subsidiaries. All financial services included in this communication are authorised by Evidentia Financial Services Pty Ltd ACN 664 546 525 AFSL 546217. It is general information only and does not constitute financial product advice. If any statements made (either alone or together) constitute advice, then the advice is general advice only and does not take into account anyone’s objectives, financial situation or needs. Before making an investment decision based on this material you should consider whether it is appropriate to your particular circumstances. Where the material relates to the acquisition or possible acquisition of a financial product, you should obtain a disclosure document relating to the product and consider the content before making any decision about whether to acquire the product. Please refer to your financial adviser for further details and any disclosure documents relevant to you. This document is based on information considered to be reliable. It is based on our judgement at the time of issue and is subject to change. No representation, warranty or undertaking is given or made in relation to the accuracy or completeness of the information presented in this document. Except for liability that cannot be excluded, Evidentia, its directors, employees, agents, and related bodies corporate disclaim all liability in respect of any error or inaccuracy in, or omission from, this document and any person’s reliance on it. This material is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. If this document contains any performance data, then performance is not a reliable indicator of future performance.

Economic shifts tend to create a ripple effect across different industries, so it can really matter to stay informed and plan a little more carefully too. Whether rates are rising or dropping, having a clear strategy can help lower uncertainty and also improve longer-term results. The same basic idea shows up when you’re working on a realtor business plan, where learning the market conditions along with the financial trends can play a major part in what happens next, and in stability later.